Introduction

The Corporate Sustainability Reporting Directive (CSRD) is European Union (EU) legislation that mandates sustainability reporting for public and private companies. It supports the European Green Deal initiatives and replaces the Non-Financial Reporting Directive (NFRD) to expand the scope and digitise sustainability reporting.

Important Acronyms

| Category | Acronym | Full Form / Description |

| Legislation |

CSRD |

Corporate Sustainability Reporting Directive |

|

NFRD |

Non-Financial Reporting Directive |

|

|

SFDR |

Sustainable Finance Reporting Directive |

|

|

Data, format and standards |

ESEF |

European Single Electronic Format |

|

ESRS |

||

|

GRI |

Global Reporting Initiative (also an organisation) |

|

|

IFRS |

International Financial Reporting Standards |

|

|

iXBRL |

||

|

ESG |

Environmental, Social and Governance |

|

|

Organisations |

EFRAG |

European Financial Reporting Advisory Group |

|

ES MA |

European Securities and Markets Authority |

|

|

NCA |

National Competent Authority |

|

|

ISSB |

International Sustainability Standards Board |

|

|

IASB |

International Accounting Standards Board |

|

|

SME |

Small and Medium Enterprises |

Main Requirements

The main disclosure requirements for the new corporate sustainability reporting are those related to relevant policies, outcomes and risks. These are described in the European Sustainability Reporting Standards (ESRS) – a set of detailed reporting requirements that companies must follow.

In addition to ESRS, CSRD also contains reporting requirements relevant to the Sustainable Finance Disclosure Regulation (SFDR). These disclose the alignment of the company’s business model to environmentally sustainable economic activities. Green activities are described in the classification system defined in the EU Taxonomy legislation – this additional reporting is commonly known as the “Article 8” sustainability report.

The CSRD says that companies must disclose sustainability information in the management report section of their annual report. It further describes how the report must be published using the European Single Electronic Format (ESEF), also know as inline XBRL (iXBRL).

European Sustainability Reporting Standards (ESRS)

The ESRS are the reporting requirements for a CSRD report. They are created by the European Financial Reporting Advisory Group (EFRAG) as a set of disclosure standards. Each disclosure standard details the sustainability information that must be published across several different sustainability topics. The disclosure standards are also published in digital format as an XBRL taxonomy.

The combination of the disclosure standards and the requirement to publish a digital report gives the common reporting framework for all companies subject to the CSRD. This framework is designed to deliver transparent and comparable sustainability information for thousands of companies covering all EU member states.

Inside Out and Outside In

A core difference between different sustainability standards is how companies need to decide whether any specific matter should be reported. This is a test for materiality and is a familiar concept in financial reporting. Materiality tests are an important part of reporting sustainability performance within the stringent reporting requirements laid down in the CSRD.

In a different set of sustainability standards, those published by the International Sustainability Standards Board (ISSB), reporting is only required if sustainability issues affect the value of the reporting company, this is often described as an “outside in” view or single materiality. On the other hand, CSRD also considers the impacts a companies activity has on the environment and people external to the company, this is described as an “inside out and outside in” view or double materiality.

The official guidance on the materiality assessment says companies must report:

“All sustainability matters affected by or that have an effect on the undertaking”

The first task for a company that falls under CSRD is to identify sustainability related risks using the inside out and outside in approach to materiality. Understanding the external sustainability issues their activities may cause and identifying other stakeholders is a major challenge for all companies doing sustainability reporting.

Why Was The CSRD Adopted?

The CSRD is explicitly tied to the European Green Deal, the EU’s response to climate change and the blueprint for how the EU will transition to net zero. In implementing the Green Deal, the EU are implementing policies, initiatives, regulations and incentives. These all have one thing in common – they require data.

For example, the new green bond standard will be used to help asset managers and other financial market participants identify sustainable companies. It will also guide the EU’s own sustainable finance initiatives to help the transition to a sustainable economy and drive economic growth. This makes corporate sustainability an important part of the financial system and whether a company meets the standard will be decided in large part by their CSRD disclosures.

Image © European Union, 2021

Consumer-level decision making is also important to drive green behaviour in company boards and their business partners. Informed consumers needs transparency and comparability between companies to make decisions that incentivise sustainable business models and make sustainable activities more profitable. Again, this can be driven by CSRD data.

The aim of the CSRD is to meet this growing demand for sustainability data and make management reports the primary source for sustainability data. Reported information will be published in the upcoming European Single Access Point, which can be used to access financial and non-financial information for thousands of public and private companies.

Non Financial Reporting Directive (NFRD)

The CSRD legislation is sister legislation to the Non Financial Reporting Directive (NFRD). The NFRD was the first major effort of the EU to ensure that companies listed on regulated markets were providing sufficient sustainability data to enable identification of sustainable investments using non financial indicators.

The public interest companies currently subject to the NFRD will be the first to transition to CSRD reporting. While not technically replacing the existing legislation, the substantial changes to sustainability reporting in the CSRD means that it effectively supersedes NFRD reporting for large companies.

Setting a Higher Bar

The CSRD raises the bar for EU sustainability reporting standards.

Firstly, the availability of data will be increased and improved through broader applicability of sustainability reporting. Previously, sustainability reporting applied only to large public interest entities, once fully running, CSRD means that sustainability information will be found in the management reports of some 50,000 companies.

Second, the comparability and transparency of information will be improved through use of digital reporting. By mandating tagged reports using the electronically readable ESEF/iXBRL format, narrative and figures are more easily analysed and processed by computers. EFRAG have also incorporated several anti-greenwashing features, such as semi-narrative disclosures into the digital reporting standard.

Perhaps most impactful, both in terms of difficulty and value is the move to double materiality. This approach, along with the more detailed reporting requirements, gives a much improved view of a company’s governance and how socially and environmentally sustainable it is.

Who Does The CSRD Apply To?

CSRD applies to approximately 50,000 EU companies that fall into any of the below categories:

- all large companies, public or private

- small and medium enterprises listed on a regulated exchange

- parent companies of a large group

These criteria follow the definitions of size category given in EU financial statement legislation. A company fits a size category when two of three size-related limits are not exceeded:

- Micro: balance sheet (€350,000), net turnover (€700,000), employees (10)

- Small: balance sheet (€4 million), net turnover (€8 million), employees (50)

- Medium: balance sheet (€20 million), net turnover (€40 million), employees (250)

- Large: any company that exceeds two of the medium-sized limits is considered large

It also applies to companies outside of the European Union that derive significant revenue from a branch or subsidiary located in the EU.

Large Companies

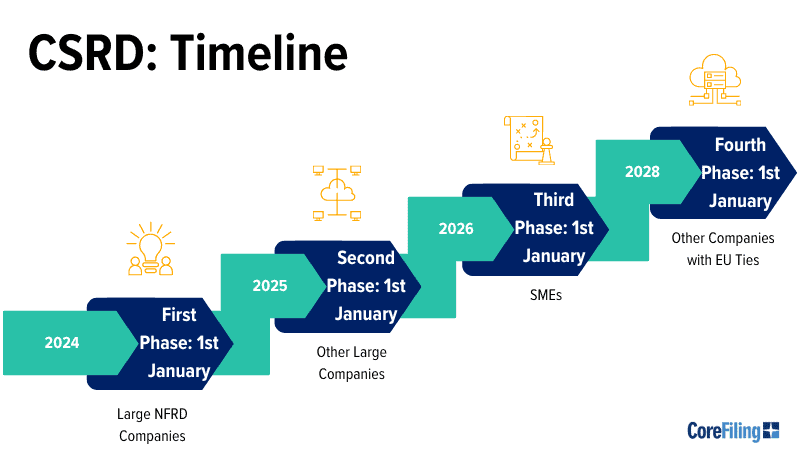

In the CSRD, large companies exceed at least two of the three medium thresholds given above. Large companies have to consider the entire reporting scope and report on any item that passes a double materiality test. In terms of deadlines, this group is split into two tranches:

1) Listed companies already subject to NFRD (and ESEF) reporting must submit their first filings in 2025 for the 2024/25 financial year.

2) Private companies not currently subject to NFRD must submit their first filings in 2026 for the 2025/26 financial year.

Small and Medium-sized Enterprises (SMEs)

If a company exceeds the thresholds for a micro-entity and does not exceed the thresholds for large companies, then they are classified as an SME. SMEs will need to use double materiality, but will be subject to proportional reporting standards. As the legislation puts in,

“proportionate to their capacities and resources, and relevant to the scale and complexity of their activities.

The first filing deadlines for SMEs is 2027 for financial year 2026/27.

Detailed Disclosures Under the CSRD

While the CSRD’s reporting standards are detailed and can seem a little daunting, the reporting requirements are split into topics and then disclosure standards, each of which are designed such that they can be considered separately. There are twelve disclosure standards in total covering covering four top level topics.

| Summary of ESRS Standards | ESRS Topics | Total Number of DR per ED |

| Panel 1: ESRS 1 | General principles | – |

| Panel 2: ESRS 2 | General, strategy, governance and materiality assessment |

12 |

| Total General | 12 | |

| Panel 3: ESRS E1 | Climate change | 9 |

| Panel 4: ESRS E2 | Pollution | 6 |

| Panel 5: ESRS E3 | Water and marine resources | 5 |

| Panel 6: ESRS E4 | Biodiversity and ecosystems | 6 |

| Panel 7: ESRS E5 | Resource use and circular economy | 6 |

| Total Environment |

32 | |

| Panel 8: ESRS S1 | Own workforce | 17 |

| Panel 9: ESRS S2 | Workers in the value chain | 5 |

| Panel 12: ESRS G1 | Affected Communities | 5 |

| Panel 10: ESRS S3 | Consumers and end-users | 5 |

| Total Social | 32 | |

| Panel 11: ESRS S4 | Business conduct | 6 |

| Total Governance | 6 | |

| Total | 82 |

The disclosure standards have been digitised to give more than 4,250 reportable items in the XBRL taxonomy. The taxonomy is designed to closely match the ESRS disclosure standards and the layout of the taxonomy should be used as a guide as to how to layout the contents of a CSRD report.

What We Know About The CSRD’s Requirements

We find it easiest to think of the CSRD’s requirements in the following way:

Data: The data required for CSRD is described in the ESRS documentation and defined as a hierarchy of data points in the ESRS XBRL taxonomy. All the data for material topics must be sourced, processed and prepared to match the data points in the taxonomy.

Format: Once the data is prepared, the whole annual report must be converted to the European Single Electronic Format, also known as iXBRL. This is usually done by starting with the final version in PDF, EPUB (an InDesign export format) or Word formats and using iXBRL tagging software to convert and tag the document to iXBRL.

Audit: Once the full annual report is complete, management reports for CSRD are subject to limited assurance to be carried out by independent assurance services providers. The exact assurance and audit requirements will vary from country to country, however, assurance can be expected to include technical checks for compliance and to ensure the computer readable tags match their presentation of the report.

Preparing Your Business for the CSRD

While many companies have been publishing sustainability reports, often voluntarily, for years, it will be new to thousands of others and require strategic planning. Many will find that this type of data may never been seen in the CFO’s office before. Below we share some good, practical steps preparing for CSRD that we see taken by our partners and customers.

Verify the scope of CSRD for your company. The timing, scope and data collector for CSRD reporting depends on several factors related to the company structure, location of incorporation and branches, where your turnover comes from, net turnover and other size-related metrics. Figuring this out and writing it down creates a reference that you can use and share whenever needed.

Identify the data. You will need to make a materiality assessment for each part of the ESRS, listing the and then finding the equivalent data points in the XBRL taxonomy gives you a bounded problem to solve. Then comes the hard part of finding where the data lives and how it must be prepared for reporting.

Track progress of the CSRD implementation. CSRD is both new and far reaching and changes should be expected, these may be in the data standards and XBRL taxonomy, assurance standards, filing rules, applicability or any of the other factors that make up a complex reporting requirement. You can track CSRD news on your national supervisor’s website and early warning of changes can be found at EFRAG and ESMA.

Finally, and while it may seem like a small thing, all of government, reporting and sustainability are notorious for acronyms! A lot of time and questions are saved by collecting all those that are relevant to you.

How Can You Become CSRD-Compliant?

CoreFiling and our partners are all working hard to take the pain out of CSRD, providing solutions for ESG management, data collection, data management, data preparation and reporting.

We currently provide software and services to the entire ecosystem of standards-setters, European and national government agencies, auditors, ESG software providers, accountancy firms, tagging providers and direct to filers. CoreFiling are chosen for our easy to use software, close attention to detail and dedication to the standards – we even invented the iXBRL format used for reporting!

This holistic view is unique and places CoreFiling right in the middle of the solution. Contact us to find out more and quickly move to full CSRD compliance.

Frequently Asked Questions

Here are some questions people want answered about the CSRD.

What Happens If My Company Does Not Comply With The CSRD?

The CSRD puts responsibility for enforcing compliance firmly with the national competent authorities (usually the securities regulator in each country). Therefore, any penalties for non-compliance are defined separately by each country during the transposition of the CSRD into national company law. The European Securities and Markets Authority (ESMA) has responsibility to promote convergence of the supervision, including non-compliance penalties, through the publication of supervisory guidance.

While there will be differences between countries, most will apply criminal sanctions in the case of non-compliance. This may include fines or prison, with audit-related failures carrying greater weight than those related to disclosure non-compliance. Companies may also be prevented from participating in public tenders and other penalties may be applied.

Are There Resources Available To Help My Company Prepare For CSRD Compliance?

How Does The CSRD Impact Companies Outside Of The EU?