Introduction

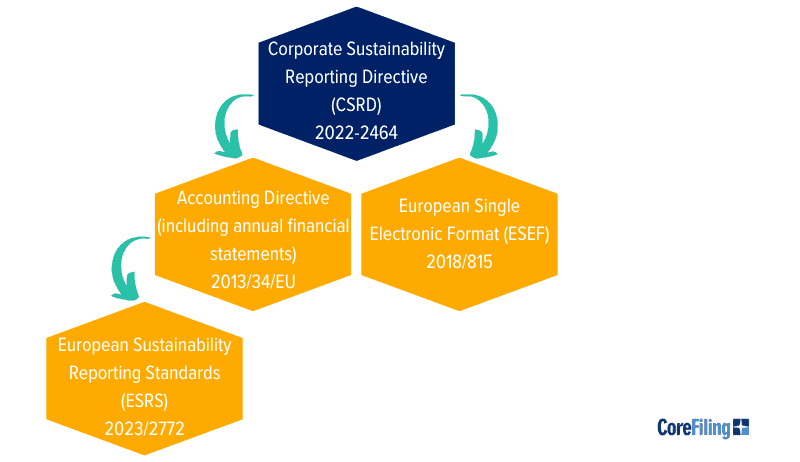

The European Commission has adopted the European Sustainability Reporting Standards (ESRS) as a core component of the Corporate Sustainability Reporting Directive (CSRD). These two acronyms are quickly becoming some of the most important in the corporate world.

Written in to European Union (EU) legislation, the ESRS is a sustainability data standard. It provides the dictionary, guidebook and detailed disclosure requirements for how to measure and disclose the sustainability of companies and their activities and, ultimately, help drive the EU’s transition to net-zero. The ESRS is authored by the European Financial Reporting Advisory Group (EFRAG), who have expanded their remit from endorsing financial reporting standards to being a standard-setter in their own right.

Without CSRD, companies needing or wanting to make statements on governance, social and environmental issues have had to choose from a multitude of reporting standards. The ESRS formalises all sustainability reporting requirements in a single EU standard and harmonises sustainability reporting for the thousands of companies subject to the CSRD.

Government, financial institutions, capital markets, consumers and even employees can be expected to take an interest in the resulting sustainability information. So companies who learn about the standards early and start to manage their sustainability in accordance with the mandatory disclosures should be able to rise above the competition, attract more people and more profits.

In this article, we cover the basic structure of the ESRS disclosure requirements, how it is used, who it applies to and the benefits you can gain by being on top of this major corporate legislation.

What are European Sustainability Reporting Standards (ESRS)?

The ESRS describe the set of sustainability-related mandatory disclosures required to meet reporting requirements under the CSRD legislation. They are to sustainability reporting what standards such as the International Financial Reporting Standards (IFRS) are to financial reporting.

Who Must Disclose?

The ESRS is explicitly written to support the CSRD which also describes the applicability of the reporting standard. In brief, the legislation mandates reporting, using the disclosure requirements in the ESRS, for approximately 50,000 EU companies and thousands of non-EU companies who derive significant revenue from subsidiaries or branches within the EU.

The reporting requirements are phased in across different groups of companies. In the first year of reporting (submission in 2025), only large, listed companies are subject to the CSRD. Non-EU companies are the last to come into scope with their first disclosure deadline in 2029.

A knock on effect of disclosure requirements relating to a company’s value chain is that companies not directly subject to the CSRD may also need to understand the ESRS. For example, the reporting company must try to get relevant and accurate sustainability information about their suppliers which can be used in reporting.

Disclosure Requirements

The ESRS disclosure requirements are published in text format in the legislation and, digitally, in the ESRS XBRL taxonomy. The legislative text gives the canonical reporting requirements, however, in practical terms, the digital taxonomy and the tagging applied in the iXBRL report will be the primary method by which compliance with the disclosure requirements is judged.

The ESRS XBRL taxonomy follows the text of the ESRS closely and will be instantly recognisable to those familiar with the content of the standard. EFRAG have stated it is reasonable to use the taxonomy as a template for a company’s sustainability statement to ensure compliance. It is standard practice for larger companies to use specialist software to prepare their disclosures.

Similarly to the phase in of companies in scope, additional phase-ins provisions apply to the disclosure requirements. The European Commission has agreed to different phase in provisions for different sized companies. For example, all companies can elect not to report value chain metrics until the third year of disclosure, whereas, scope 3 greenhouse emissions data may only be omitted in the first year if the company has fewer than 750 employees. Appendix C in the General Requirements part of the ESRS delegated act is a list of all phased-in disclosure requirements and their applicability.

Summary of the phase-in (full version is in table in “Appendix C: List of phased-in Disclosure Requirements” here, also see this page for example: WordPress)

The Draft ESRS

The draft ESRS was published in April 2022 and the final ESRS was published as a delegated act in July 2023. A delegated act has a lightweight legal process in order to amend more specific information about a piece of general legislation to a piece of EU law (in this case, the CSRD). Further delegated acts will be published to handle sector specific standards and proportionate standards for SMEs in due course.

When the draft standards were released, EFRAG published the draft standards in an easy to consume set of ESRS Exposure Drafts. They also published technical advice and high level explanations of the disclosure requirements. While the draft ESRS was amended following public consultation, the information released remains a good starting point to understand the contents of a CSRD report.

Sustainability Reporting: How ESRS Works

The ESRS is an example of principle-based reporting which describes the complete set of in-scope sustainability disclosures. The actual disclosures that need to be made are those that pass a materiality assessment, carried out by the reporting company. The structure of the ESRS and application of double materiality are discussed in more detail below.

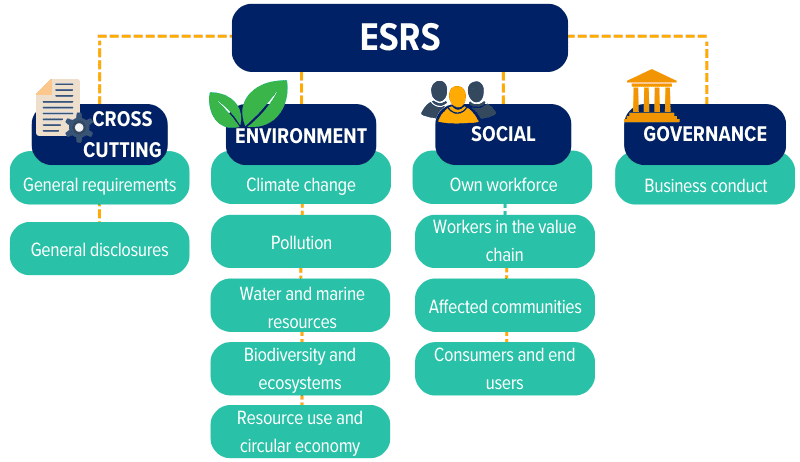

The ESRS has twelve sets of disclosure standards, there are two cross-cutting standards and ten topical standards. The cross-cutting standards are general disclosures and are used to report sustainability information relevant to all companies. The topical standards cover Environment, Social and Governance standards which are further broken down into topics (e.g. Climate change is a topic of the Environment standards).

Each topic has its own self-contained section in the ESRS. Each section contains a description of the disclosure objective, a number of disclosure standards and, finally, a set of application requirements. The application requirements give further instructions on how to meet the disclosure requirements.

The disclosures themselves generally fall into one of the below categories:

-

Process descriptions

-

Impact, risk and opportunities (IROs)

-

Policies, actions and targets (PATs)

-

Metrics

Cross-cutting matters must be reported by every company whereas topical disclosures are subject to a double materiality assessment (impact and financial). The EFRAG has published non-binding implementation guidance specifically on the topic of how to carry out a materiality assessment. Also, the upcoming Corporate Sustainability Due Diligence Directive (CSDDD/CS3D) will introduce legislation relevant to materiality assessments for very large companies.

For materiality assessments, it is also important to distinguish between disclosure standards that relate directly to a company’s own operations and those that relate to the entire value chain. The EFRAG has published further implementation guidance that specifies essential information around how to assess materiality in the value chain.

“A value chain encompasses the activities, resources and relationships the undertaking uses and relies on to create its products or services from conception to delivery, consumption and end-of-life.” – EFRAG IG 2: Value chain

The EFRAG also cites the Global reporting initiative (GRI) standards as a good basis for the assessment of impact. The “GRI 3: Material Topics” standard (available on the GRI website) contains a detailed explanation on how to carry out an assessment.

Environmental Standards

The first thing people often think of when it comes to sustainability is the impact on the environment. The ESRS splits the disclosure requirements for environmental standards into five topics:

-

Climate change: climate related disclosures including energy usage and adaptation and mitigation related to climate change

-

Pollution: Pollution of air, water, soil, living organisms and food as well as substances of concern and microplastics

-

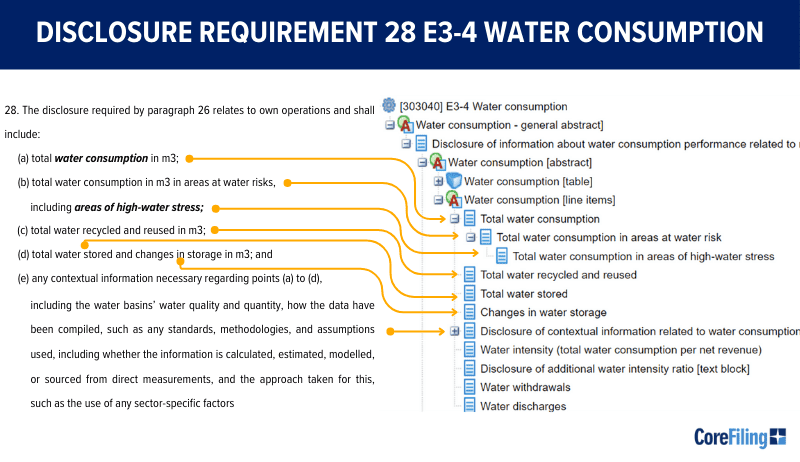

Water and marine resources: Water consumption, withdrawal, discharges and extraction and use of marine resources

-

Biodiversity and ecosystems: Direct impact drivers on biodiversity loss, state of species and the extent, condition, impacts and dependencies of ecosystems

-

Resource use and circular economy: Resource inflows and outflows as well as waste handling

The EFRAG has collaborated with several other organisations to develop the disclosures for the environment topic, including the GRI, the Taskforce on Nature-related Financial Disclosures (TNFD) and the Carbon Disclosure Project (CDP).

Social Standards

Social standards concern the impact on people, their working conditions, personal safety, training, opportunities and also cover diversity and equality matters. They cover those working for the company, those working at suppliers and impacts on consumers of the company’s services or products as well as people affected in other ways by the company’s activities.

The ESRS breaks down social standards into four topics:

-

Own workforce: Working conditions, equality and workers’ rights for the company’s workforce

-

Workers in the value chain: Working conditions, equality and workers’ rights in companies in the value chain

-

Affected communities: The rights of indigenous people and other communities affected by the company activities

-

Consumers and end users: The safety, social inclusion and information-related impacts for consumer and/or end users

Governance Standards

In sustainability, governance concerns good practices to ensure the continuity of business and ethical behaviour. There is a single topic for governance – Business conduct.

Business conduct covers corporate culture, protection of whistle-blowers, animal welfare, political engagement, management of suppliers and corruption.

Preparing for ESRS

In practical terms, the standards themselves and the materiality guidelines from ESMA give a great starting point for companies. Software can help a lot to move further on in the process, tracking materiality assessments and helping you bring together the data required as well as producing the report in the correct format.

It is important to socialise the message that reporting on sustainability matters is public and will be published for consumption by a broad range of interested parties. An increase in sustainability awareness and increased use of sustainability data to influence the decisions of financial markets and consumers is the explicit goal of CSRD. Also, while currently only reporting on sustainability issues is mandated, the legislation needs to be understood as part of an overall plan to make Europe a sustainable economy with incentives and regulations based on the data points reported.

People take views as to the long term sustainability of your operations and how the company is run based on corporate reporting. Starting to manage sustainability metrics means that you are not left behind in an increasingly sustainability-aware world.

Global Standard Setting Initiatives

A challenge when coming up with a new data standard, is these are not new and there are already many initiatives and standards filling the role partially or completely. Competition between standards may help them develop, but the resulting data is more useful if it is directly comparable. In order to handle this challenge, the EFRAG has collaborated with multiple organisations, not least of which IFRS who themselves have merged and signed memorandums of understanding (MOUs) with several of the existing standard setters to bring them under one banner.

Out of this also comes the idea of mapping between standards to enable people to better report and better compare in the cases where legislation calls for different base reporting principles. The IFRS has released a mapping sheet to give a detailed view of similarities and differences between the two standards, and can be used to align and simplify the identification of items to report.

Differences: ESRS, NFRD, ISSB, GRI

In the table below, we highlight the major differences between well known sustainability standards that cover the full range of environment, social and governance (ESG) areas. Note that there are other related standards that have a narrower scope and may be jurisdictions-specific, these include Streamlined Energy and Carbon Reporting (SECR) in the UK and Climate Related Disclosures in the US.

-

European Sustainability Reporting Standards (ESRS): new EU sustainability reporting standard

-

Non-Financial Reporting Directive (NFRD): previous EU sustainability reporting standard

-

International Sustainability Standards Board (ISSB): ISSB standards aim to give the global baseline for sustainability reporting

-

Global Reporting Initiative (GRI): the most popular global impact reporting standard

|

Feature |

ESRS |

NFRD |

ISSB |

GRI |

|

Materiality |

Financial/impact |

Financial |

Financial |

Impact |

|

Digital report size* |

1,306 items |

N/A |

723 items |

717 items |

|

Company scope** |

Large and listed |

Large listed |

Voluntary |

Voluntary |

|

Digital format |

ESEF (iXBRL) |

N/A |

iXBRL |

iXBRL |

|

Adoption |

EU |

EU |

Global |

Global |

* Indicative report size is given as the number of reportable items (non-abstract concepts) in the taxonomy

** As of July 2024

Get Help with ESRS Compliance

CoreFiling and our partners, through software and services, offer a complete solution for ESRS and broader CSRD compliance. This covers everything from full data projects to preparing and tagging the final report.

If you are ready to get started or need help getting over the line, then contact us.

Frequently Asked Questions

Below, you can find answers to common questions about the ESRS.

What Is The Purpose Of ESRS?

The purpose of the ESRS, alongside the digital disclosure requirement, is to create a standardised framework in which to report and analyse corporate sustainability.

For corporates, it contains the detailed disclosure requirements of the CSRD legislation and additional details on how these should be interpreted.

For interested parties, it delivers detailed, comparable data on a number of different topics to select investments and make consumer-based purchasing decisions.

Who Needs To Comply With ESRS?

Use of the ESRS is mandatory in disclosures required by the CSRD. This means it applies to:

-

Large public and private EU companies

-

Small and medium-sized companies listed on EU regulated exchanges

-

Large subsidiaries and branches of non-EU companies

Of course, there is nothing stopping other EU and non-EU companies outside the scope of CSRD from informing the market of their sustainability credentials by following the ESRS. Adopting the standard ensures your sustainability credentials are able to be directly compared with others.

What Are The Benefits Of ESRS For Companies?

The ESRS levels the playing field for sustainability disclosures by delivering comparable data points rather than general narrative. It ensures that efforts to improve environmental, social and governance matters can be communicated effectively with stakeholders and will be the basis on which companies prove they qualify for sustainability-related initiatives.

Not only will an ESRS help communicate to others, but it may make you look at your company in a different way and see how you can improve your company.

The benefits are such that some have already started creating sustainability reports using draft standards. H+H International is just one of these companies.