Introduction

Sustainability reporting in the European Union (EU) has evolved significantly, reflecting the growing emphasis on corporate responsibility and transparency. Businesses must understand the transition between the existing Non-Financial Reporting Directive (NFRD) and the incoming Corporate Sustainability Reporting Directive (CSRD) to make effective use of the regulations and turn them into something positive.

Historically, the EU has progressively strengthened its sustainability reporting regulations, starting with the NFRD in 2014, which mandated non-financial disclosures for large companies. The CSRD, introduced as a concept in 2021, marks another paradigm shift, broadening the scope and depth of reporting requirements to enhance corporate accountability.

This blog aims to provide a comprehensive comparison of NFRD and CSRD, highlighting the key changes and their implications, thereby equipping you with the knowledge needed to transition smoothly and uphold exemplary reporting standards.

What is the Non-Financial Reporting Directive (NFRD)?

Before we compare the two legislations, it is vital to get a working understanding of each, we start with the NFRD, which has been in effect since 2014.

Definition and Objectives of NFRD

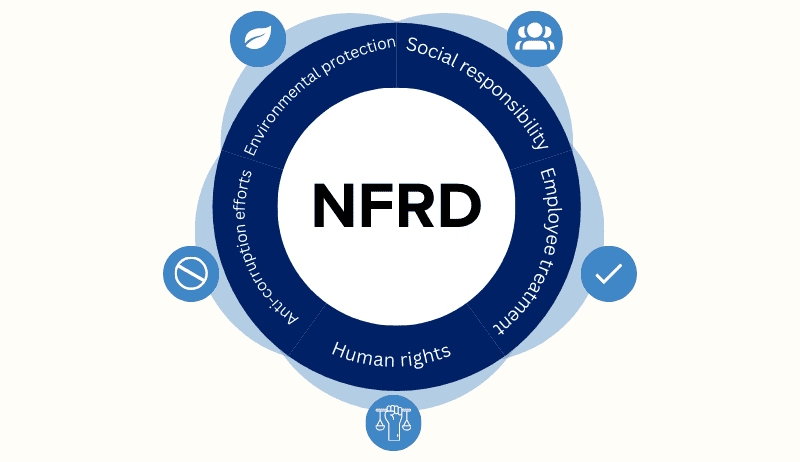

The Non-Financial Reporting Directive (NFRD), established by the European Union in 2014, mandates that large companies disclose non-financial information on social and environmental issues. This legislation came into effect in 2018, with the primary objectives of enhancing corporate transparency and accountability to cultivate sustainable and responsible business practices. Under the NFRD, companies must report on matters such as:

- Environmental protection

- Social responsibility

- Employee treatment

- Human rights

- Anti-corruption efforts

Key Aspects Of NFRD

As written in the NFRD (EU Directive 2014/95/EU), these sustainability reports aim to provide stakeholders with a comprehensive understanding of a company’s non-financial performance, thereby facilitating informed decision-making and promoting long-term sustainability.

Scope of Companies Affected

The Non-Financial Reporting Directive (NFRD) applies to large public-interest entities with over 500 employees. This includes listed companies, banks, insurance firms, and other entities designated by national authorities as public-interest entities. The NFRD’s scope ensures that the largest and most influential organisations are held accountable for their environmental and social impacts.

By focusing on these entities, the directive aims to promote greater transparency and responsible business practices across sectors, enabling stakeholders to assess the company’s sustainability performance and commitment to ethical practices effectively.

Introducing the Corporate Sustainability Reporting Directive (CSRD)

Now that we’ve summarised the current EU sustainability reporting regulations, let’s look at those which started to come into effect from 2024.

Definition and Objectives of CSRD

The Corporate Sustainability Reporting Directive (CSRD) aims to enhance and standardise sustainability reporting across the European Union. It expands the scope of reporting requirements to include more companies, ensuring greater transparency and comparability of environmental, social, and governance (ESG) data.

The CSRD mandates detailed disclosure of sustainability impacts, risks, and opportunities, aligning with the EU’s Green Deal and sustainable finance initiatives.

By improving the quality and accessibility of ESG information, the CSRD seeks to encourage sustainable business practices, facilitate stakeholder decision-making, and support the transition to a more sustainable and inclusive economy.

Key Differences Between NFRD vs CSRD

As you might have realised, the CSRD marks a significant change from existing legislation. Let’s unpack the specific ways that it differs from its predecessor.

Scope and Coverage

The Non-Financial Reporting Directive (NFRD) only affects large public-interest companies with over 500 employees. In contrast, the Corporate Sustainability Reporting Directive (CSRD) significantly broadens the scope to include all large companies and listed SMEs, impacting approximately 50,000 businesses across the EU. By 2028, the scope will also include thousands of non-EU companies which derive significant revenue from EU-based branches and subsidiaries.

Reporting Standards and Frameworks

The Corporate Sustainability Reporting Directive (CSRD) introduces several enhancements over the NFRD. It incorporates the ‘double materiality’ concept, requiring companies to report both the societal and environmental factors affecting them AND the impact of their business on environmental issues, such as climate change and resource scarcity.

Companies must publish digital, tagged reports in the European Single Electronic Format (ESEF/iXBRL) using the European Sustainability Reporting Standards (ESRS) XBRL taxonomy. In the NFRD, no digital reporting requirements were given and PDFs were typically used to communicate the information.

Firms must also conduct due diligence on their operations and supply chains and disclose information on intangibles like social, human, and intellectual capital. Reporting must align with the European Sustainability Reporting Standards (ESRS) and the EU Taxonomy Regulation.

Level of Detail in Disclosures

In terms of detail, the NFRD legislation gave no formal standards, instead preferring to give companies flexibility in how they report. The legislation covers only a couple of pages, giving a very limited number of narrative disclosures.

As the NFRD approach proved to provide insufficient detail to support demand for sustainability data, the level of detail has changed considerably. The CSRD comes with formal standards that cover general, environmental, social, and governance matters in detail. This holistic approach to sustainability reporting has resulted in hundreds of pages of standards – written into legislation – and thousands of potential data points.

Due to the broad and deep nature of the reporting obligations, the application of CSRD has several phase-in provisions and some disclosures have been made voluntary. This ensure that proportionality was achieved, especially to protect SMEs from excessive reporting burdens.

Assurance and Audit Requirements

The CSRD requires the sustainability information to be verified by an independent auditor, enhancing transparency and trust. This shift significantly increases the robustness of sustainability reporting compared to the NFRD’s more lenient approach, reflecting the growing importance of verified, high-quality non-financial disclosures in corporate reporting.

| NFRD | CSRD | |

| Scope and Coverage | Large public entities | Large companies, small and medium buisnesses, Non-EU business with significant EU ties |

| Reporting Standards and Frameworks | No restriction on method of reporting | European Single Electronic Format (ESEF/iXBRL) with data tags |

| Level of Detail in Disclosures | Information on environmental and societal impacts | Information on a comprehensive list of general, environmental, societal and governance impacts according to the European Sustainability Reporting Standards (ESRS) |

| Assurance and Audit Requirements | Flexibility and non-binding guidelines | Independent audit to determine ESRS compliance |

Impacts and Implications of the Transition from NFRD to CSRD

So, what does all this mean for you if you’re a business that fits the criteria for CSRD reporting?

Benefits for Companies and Stakeholders

Greater investor confidence and access to capital are significant advantages of the CSRD. Investors are increasingly prioritising sustainable investments, and companies demonstrating thorough sustainability practices are more likely to attract funding.

“As investors, we will engage on the topic in the spirit of open inquiry and innovation, with the goal of developing widely shared best practices that link climate-related investment, decent jobs, thriving communities and sustainable development.”

This evidence from the United Nations’ Principles for Responsible Investment supports this, showing a positive correlation between high-quality sustainability reporting and investor interest.

Challenges and Opportunities for Businesses

The transition from NFRD to CSRD presents both challenges and opportunities for businesses. One significant challenge is the increased compliance costs and administrative burden. The CSRD’s stringent European Sustainability Reporting Standards (ESRS) requirements necessitate extensive data collection and third-party verification, which can be resource intensive.

However, this challenge also presents an opportunity for businesses to integrate sustainability into their core strategy, promoting long-term resilience and competitive advantage.

Early adopters may also benefit from streamlined processes and reduced future compliance costs, establishing a strong foundation for sustainable growth.

The Last Word

The transition from NFRD to CSRD marks significant changes in scope and coverage, expanding from large public-interest companies to all large firms and listed SMEs, impacting around 50,000 businesses in the EU. CSRD also introduces enhanced reporting standards, including double materiality, coverage of long-term ESG objectives, and mandatory external assurance, ensuring more detailed and comparable information.

Early preparation is crucial for businesses to make these changes effectively and gain a competitive edge. Companies should begin preparing for CSRD now to ensure compliance and benefit from enhanced transparency and trust in their sustainability reporting.

Act now with CoreFiling and contact us to reduce compliance costs and maximise the value of CSRD to your company.

Frequently Asked Questions

Here are some common questions you may have when comparing the NFRD to the CSRD.

What Types Of Companies Are Affected By The CSRD That Were Not Covered Under The NFRD?

The CSRD extends to all large companies and listed SMEs, unlike the NFRD, which covers only large public-interest entities. Additionally, it impacts non-EU companies with substantial business in the EU, broadening the scope and ensuring comprehensive sustainability reporting across various sectors.

How Will The CSRD Impact Reporting Timelines And Cycles?

The CSRD introduces staggered timelines for compliance. Companies subject to NFRD must begin reporting in 2024, other large companies in 2025, followed by listed SMEs in 2026. Non-EU companies with substantial business in the EU are required to report by 2028. This phased approach allows businesses time to adapt to the new requirements, ensuring a smoother transition to comprehensive sustainability reporting. Whatever the size of your company, it is best to start preparing now to meet these deadlines effectively.