Introduction

The Corporate Sustainability Reporting Directive (CSRD) is already in effect for some companies and will continue to impact many more in the coming years.

As your environmental impact comes under greater scrutiny, you must understand the new regulations for EU member states and how they could affect your business.

This blog will break down the aspects of the CSRD, the reporting requirements, who needs to comply and when.

What is the Corporate Sustainability Reporting Directive (CSRD)?

The Corporate Sustainability Reporting Directive (CSRD) is a significant EU regulation aimed at enhancing and standardising sustainability reporting across companies operating within the European Union. It mandates comprehensive disclosure of environmental, social, and governance (ESG) impacts by companies, ensuring transparency and accountability.

According to the European Commission,

“The new rules will ensure that investors and other stakeholders have access to the information they need to assess the impact of companies on people and the environment and for investors to assess financial risks and opportunities arising from climate change and other sustainability issues.”

The directive is a response to increasing demands for corporate transparency and the need to align with the EU’s Green Deal objectives – no net emissions of greenhouse gases by 2050.

Differences From Previous Sustainability Reporting Standards

The CSRD builds upon the foundations laid by the Non-Financial Reporting Directive (NFRD). The Corporate Sustainability Reporting Directive (CSRD) represents an evolution from the Non-Financial Reporting Directive (NFRD).

The NFRD requires large public-interest companies to disclose non-financial information on environmental protection, social responsibility, and governance. However, its scope is limited and lacks a standardised reporting frameworks.

The CSRD, by contrast, demands detailed reporting on environmental, social, and governance (ESG) aspects and extends its scope to a much broader range of companies. It also addresses previous gaps by requiring third-party assurance and reporting information digitally, using the European Single Electronic Format (ESEF).

CSRD Reporting Requirements

The Corporate Sustainability Reporting Directive (CSRD) sets forth a comprehensive framework for sustainability performance that surpasses previous standards. Companies are required to provide detailed disclosures on general, environmental, social, and governance (ESG) factors.

Building on existing regulations, they also need to demonstrate ‘double materiality’ where they show how they are impacted in these key metrics as well as their external effect on their environment. This is often referred to as the ‘inside out’ and ‘outside in’ approach.

Key reporting elements include climate change mitigation, biodiversity protection, social and employee matters, respect for human rights, anti-corruption, and bribery issues.

-

The CSRD applies to all large companies and listed small to medium-sized enterprises (SMEs), significantly expanding the scope from the previous Non-Financial Reporting Directive (NFRD).

-

The directive introduces mandatory third-party assurance to enhance the credibility of the reported data.

-

The CSRD also mandates digital tagging to facilitate accessibility and comparability.

For an in-depth understanding of the CSRD requirements, companies can refer to the official CSRD documentation on the European Commission’s website and trusted explanatory articles.

The European Sustainability Reporting Standards (ESRS)

The European Sustainability Reporting Standards (ESRS) form the backbone of the CSRD, providing a new framework of detailed guidelines on the content and structure of sustainability reports. ESRS outlines specific disclosure requirements across various ESG dimensions, including:

-

Climate change: Mitigation and adaptation strategies.

-

Biodiversity: Conservation and sustainable use.

-

Social capital: Human rights, diversity, and inclusion.

-

Governance: Ethical business practices and anti-corruption measures.

Each standard is designed to ensure that reported information is comprehensive, comparable, and transparent.

Sustainability experts emphasise the importance of ESRS in harmonising reporting practices across the EU, thereby enhancing the quality and reliability of sustainability data. According to the official ESRS guidelines, companies must report on sustainability matters in both qualitative and quantitative aspects, ensuring a holistic view of their ESG performance.

For authoritative information, consult the European Commission’s official ESRS documents and the guidelines provided by the European Financial Reporting Advisory Group (EFRAG). These resources offer detailed explanations and updates essential for compliance and effective reporting.

Remember: Alongside the ESRS, the Sustainability Finance Disclosure Regulation (SFDR) and the EU Taxonomy “Article 8” disclosures also form part of the CSRD requirements.

It is paramount that all businesses previously subject to the NFRD and those who are mandated with sustainability reporting for the first time are well-versed in these before they start the reporting process for the key ESG metrics.

CSRD: Timeline

Now that you have a working understanding of what the CSRD is all about. Let’s take a look at the timeline for compliance, looking at the phases alongside the types of companies affected.

First Phase: 1st January 2024

-

During this phase, all large public-interest entities with over 500 employees, which were already subject to the Non-Financial Reporting Directive (NFRD), must comply with the new CSRD requirements of reporting transparently on their ESG aspects.

-

The regulation refers to financial years starting on or after this date meaning that the first compliance report will be filed in 2025.

Second Phase: 1st January 2025

-

The second phase, starting on 1st January 2025, extends CSRD compliance to large companies not previously covered under the NFRD.

-

Specifically, this includes companies with more than 250 employees and a turnover exceeding €40 million. These companies must adhere to detailed ESG reporting requirements, ensuring comprehensive and comparable sustainability disclosures.

-

This refers to financial years starting on or after this date. Therefore, the first report in 2026 will cover the entire year.

Third Phase: 1st January 2026

-

The third phase, commencing on 1st January 2026, significantly broadens the scope of CSRD to include listed small and medium-sized enterprises (SMEs) for the first time.

-

Experts highlight that this phase will allow for greater transparency and accountability among a wider range of businesses, driving sustainable practices across various sectors.

-

Again, this phase means a report will be necessary in 2027 to cover the 2026 financial year.

Fourth Phase: 1st January 2028

-

The final phase, starting on 1st January 2028, marks the full implementation of the CSRD, encompassing all remaining companies within its scope, including companies with a net turnover exceeding €150 million within the EU and at least one subsidiary or branch meeting specific thresholds.

-

This phase aims to ensure universal adherence to comprehensive ESG reporting standards, significantly enhancing transparency and sustainability practices across the EU.

-

Once more there will be a report in 2029, to reflect the 2028 financial year.

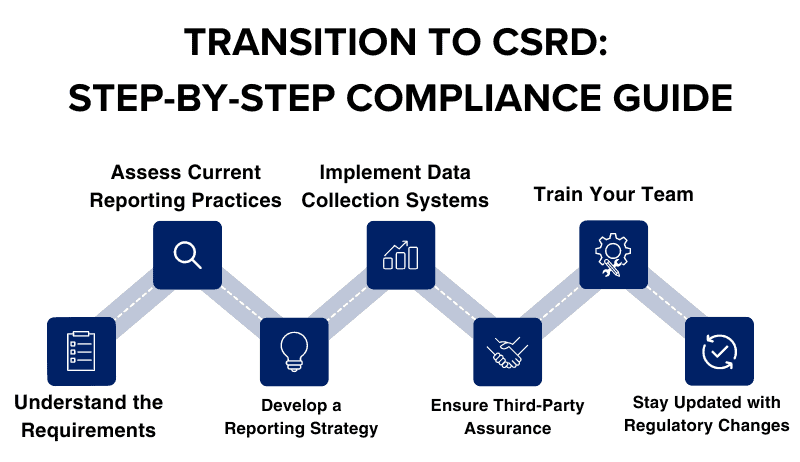

Transition to CSRD: Step-By-Step Compliance Guide

So now you know where you fit into the CSRD timeline. But how can you ensure a smooth transition for your business?

Understand the Requirements: Familiarise yourself with the CSRD and its detailed reporting standards. Refer to the European Commission’s official documentation and the legislation itself for comprehensive insights.

Assess Current Reporting Practices: Conduct a gap analysis to evaluate your existing reporting against CSRD requirements. Identify areas that need enhancement, particularly in ESG metrics.

Develop a Reporting Strategy: Establish a clear strategy for gathering, verifying, and reporting ESG data. Engage key stakeholders across your organisation to ensure alignment and support.

Implement Data Collection Systems: Invest in state-of-the-art data management systems to collect and analyse sustainability data. Ensure these systems are capable of providing accurate and verifiable information. Speak to us for more information about this.

Ensure Third-Party Assurance: The CSRD mandates third-party verification of sustainability reports. Engage a reputable assurance provider to review and validate your data.

Train Your Team: Provide training to your reporting team on the new requirements and data management practices. Utilise resources from leading sustainability consultants to stay informed about best practices.

Stay Updated with Regulatory Changes: CSRD guidelines may evolve. Regularly consult official guidance documents and compliance toolkits to ensure ongoing compliance.

Following these steps will help your business conduct your organisation meet CSRD requirements and enhance your sustainability reporting practices.

Conclusion

The Corporate Sustainability Reporting Directive (CSRD) represents a monumental shift in global sustainability reporting. By mandating comprehensive ESG disclosures, the CSRD aims to enhance transparency and accountability across the corporate sector and extending beyond the EU.

The legislation is not just a burden, but also an opportunity. EU incentives will mean companies are financially better off if they are able to communicate the steps they are taking to reach net zero and other positive impacts their activities have. Aside from the external factors, it also gives a framework on which to reflect on the operation of the company to plan for the long term and with a positive sustainability outlook.

The CSRD sets a new global benchmark for the quality and content of ESG reporting, driving significant environmental and social benefits. To stay competitive, companies worldwide must align with these rigorous standards and begin reporting to these timelines, embracing transparency and sustainable practices. If you need any more advice about how and when you should comply, CoreFiling is on hand to help.

Frequently Asked Questions

We’ve answered some frequently asked questions related to the CSRD timeline that could affect your business in the coming years.

What Companies Are Required To Comply With CSRD?

The CSRD applies to all large companies operating within the European Union, defined as those meeting at least two of the following criteria: more than 250 employees, a net turnover exceeding €40 million, or a balance sheet with total assets of over €20 million. Additionally, listed small and medium-sized enterprises (SMEs) and non-EU companies with a net turnover of more than €150 million in the EU and at least one subsidiary or branch exceeding specific thresholds are also included.

How Does The CSRD Differ From Other Sustainability Reporting Standards?

The CSRD distinguishes itself by mandating comprehensive, standardised ESG reporting for a wider range of companies, including detailed requirements on environmental, social, and governance factors. Unlike previous standards like the Non-Financial Reporting Directive (NFRD), the CSRD requires third-party assurance and digital tagging of reported information, enhancing transparency and comparability.

What Are The Consequences Of Non-Compliance With The CSRD?

Non-compliance with the CSRD can lead to significant legal and financial repercussions. Companies may face substantial fines and penalties imposed by national regulatory bodies. Failure to comply can damage a company’s reputation, leading to a loss of investor trust and potential financial instability. According to the European Commission, enforcement policies include regular audits and stringent penalties for inaccurate or incomplete reporting.